What Are the Different Types of Funds in Government Accounting?

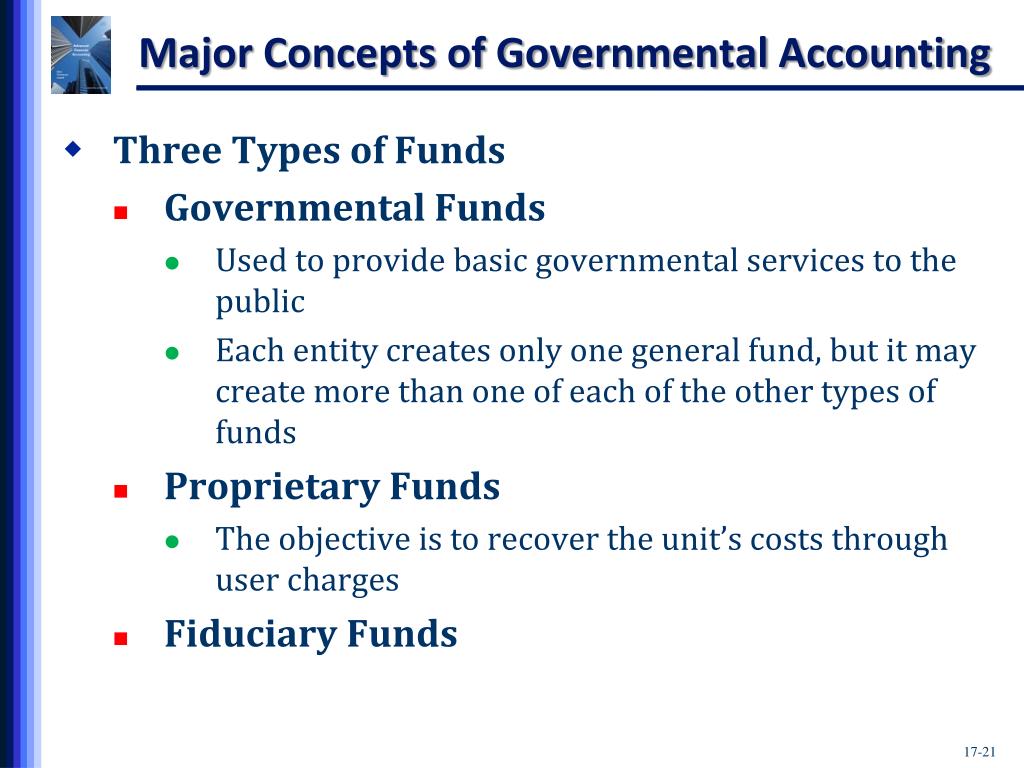

The fiduciary fund category consists of funds where the government is serving as a trustee or custodian of resources for citizens, organizations, or other governmental entities. The government is restricted from using the funds, but holds them for a specific group, entity or activity. Common examples of fiduciary funds are pensions or other types of employee benefit funds. Governmental funds are one of the primary types of funds used by governmental entities to account for resources that are typically derived from tax revenues and other public sources. The main purpose of governmental funds is to track the inflow and outflow of money necessary to support governmental services and ensure the public accountability of government finances.

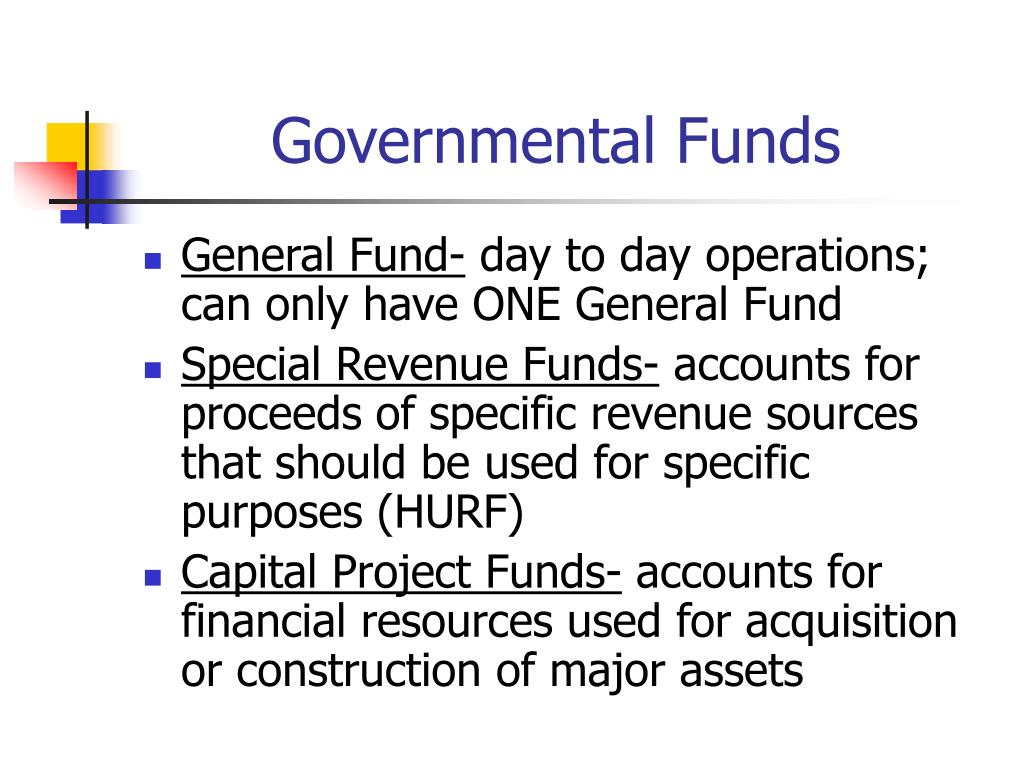

Capital Projects Funds

If you are just entering the realm of grants and government funding, it can feel overwhelming trying to find the right program for you or your organization. When considering grants, these programs can be broadly categorized as those awarded by the federal government and those awarded by non-federal entities. Although some major legislative proposals could significantly affect the economy—by affecting consumer prices or the labor supply, for example—most would not. By long-standing convention, CBO’s cost estimates typically do not account for the possible effects of legislation on GDP. Occasionally, however, the Congress asks CBO to provide a dynamic analysis of proposed legislation.

Government Fund Accounting: Types of Funds and Leases under GASB 87 w/ Journal Entries

- The determination of an activity’s principal revenue source is a matter of professional judgement.

- Although FCRA accounting is required by law to be used for recording outlays in the budget, fair-value accounting can be used to analyze credit programs, insurance programs, and retirement benefits.

- At each layer, the definition and display provisions should be applied before the layer is included in the financial statements of the next level of the reporting government.

- Lastly, each type of fund addresses specific community needs—from everyday municipal operations covered by governmental funds to business-like activities addressed by proprietary funds, and specific fiduciary responsibilities managed through fiduciary funds.

Cost-of-living adjustments for Social Security and other programs, for example, are set on a calendar year basis. In addition, individual income taxes are levied on a calendar year basis, and economic data are typically reported for calendar years. Cost estimates explain how legislation would change federal spending and revenues over the next 5 or 10 years in relation to CBO’s projections of budgetary outcomes under current law.

Budgeting

Federal financial assistance is a broad term to refer to the various ways the U.S. government redistributes resources to eligible recipients. On Grants.gov you will find grant and cooperative agreement opportunities from federal agencies that award grants. Applicants must provide evidence that they are an incorporated entity by providing types of governmental funds either an Australian Business Number (ABN) or an Australian Company Number (ACN). Expenditures should be classified by fund, function (or program), organization unit, activity, character, and principal classes of objects. Transfers should be reported in the accounting period in which the interfund receivable and payable arise.

In fund accounting, government finances are categorized into various funds based on the activities they support, the sources of funding, and the rules that apply to their use. This categorization allows government entities to manage and monitor resources more effectively, ensuring transparency and adherence to legal and financial policies. Looking forward, fund accounting will continue to play a critical role in adapting to changing financial landscapes and increasing public demands for transparency and accountability. As technology advances, we can expect more sophisticated financial management systems that provide real-time data analysis and enhanced reporting capabilities.

LEGAL

Only the interest that is generated from the principal amount can be disbursed as returns for the cause. The general fund is used as a medium to account for respective different heads that are used in order to note all the related expenses in the respective accounting heads. (a) Government-wide financial statements.(b) Fund financial statements.(c) Notes to the financial statements. SAM.gov Assistance Listings is the authoritative source of information about federal programs that provide grants, loans, scholarships, insurance, and other types of assistance awards. Reappropriations extend the originally specified period of availability for unused budget authority that has expired or that would otherwise expire. Generally, that reappropriated budget authority is for the originally stated purpose, but sometimes it can be used for a different purpose.

When the major fund criteria are applied to governmental funds, revenues do not include other financing sources and expenditures do not include other financing uses. Transparency is further enhanced by the strict reporting standards required for each type of fund. Governmental, proprietary, and fiduciary funds each have unique reporting requirements that align with their operations and objectives, as dictated by regulatory bodies like the Governmental Accounting Standards Board (GASB). Code Fiduciary Funds – should be used to account for assets, including capital assets (GASB 34, Paragraph 106), held by a government in a trustee capacity or as a custodian for individuals, private organizations, other governmental units, and/or other funds. These include (a) investment trust funds, (b) pension (and other employee benefit) trust funds, (c) private-purpose trust funds, and (d) custodial funds. Code Special Revenue Funds – should be used to account for and report the proceeds of specific revenue sources that are restricted or committed to expenditure for specific purposes other than debt service or capital projects.

Therefore, it mainly accounts for infrastructure-related costs that are borne by the government. Therefore, they mainly include costs pertaining to significant capital expenditures that are undertaken, and this fund only holds reserves for this particular cause. Government funds can be categorized into different types, each designed to handle specific financial activities and objectives.

If the resources are initially received in another fund, such as the general fund, and subsequently remitted to a special revenue fund, they should not be recognized as revenue in the fund initially receiving them. They should be recognized as revenue in the special revenue fund from which they will be expended. Code General (Current Expense) Fund – should be used to account for and report all financial resources not accounted for and reported in another fund. Federal Government by providing information on state and federal agencies and programs. It also facilitates access to the benefits and services for which you may be eligible, including personal funding. Although most federal programs operate on a fiscal year basis, some aspects of programs are set to the calendar year.